{kind=link}

Did I say mandatory? I meant optional! You’re “free” to die in a cardboard box under a freeway as a market capitalist scarecrow warning to the other ants so they keep showing up to make us more!

Did I say mandatory? I meant optional! You’re “free” to die in a cardboard box under a freeway as a market capitalist scarecrow warning to the other ants so they keep showing up to make us more!

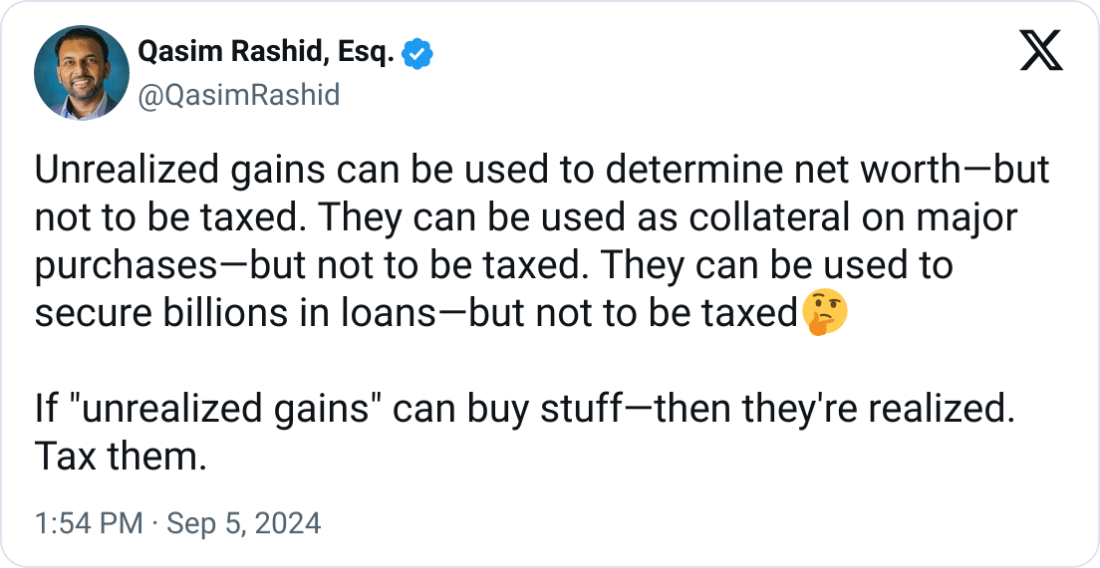

This isn’t about borrowing against assets. I’m fine if that’s taxable.

This is about holding a stock and paying tax just for owning it despite it might be worthless when you go to sell it.

But you can already deduct losses from your taxes, up to $3,000 per year and if you have more than that, you can carry it forward. If it’s worthless when you sell, you can deduct all of the loss from your taxes.

If paying a large amount of taxes on money you didn’t make today because you can save a little money on taxes later makes sense, then I have a deal for you:

You give me $60k today and I agree to pay you back $3,000 a year until you’ve got that $60k back.

Stocks can and do frequently spike for a year or two just because the public has a fad. The stock goes back to the price you paid for it. You don’t have any losses when selling. You paid taxes on money you don’t have.

You’re just throwing random numbers around. Stocks generally aren’t that volatile, but when they do rise and fall quickly there’s usually a reason.

Like let’s say you bought GameStop stock, and it experiences extreme volatility. Let’s keep the math easy and say you start with 100 shares of stock worth $10k total, and the stock jumps to $100k. Having diamond hands, you don’t want to sell, but you owe 28% of the $90k you “made” on the stock, which can be spread out over 9 years. You sell $2,800 worth of stock this year, and you’re left with $97,200. The next year, the stock tanks to it’s original value. You have $9,720 in stock, and you have a $2,800 prepaid tax credit for whenever you decide to sell the stock. The next year, the company goes bankrupt and dissolves. You have a $10,000 loss which you can deduct from taxable income over four years, and a $2,800 tax credit.

Two things are important in this example: Such taxes only apply to individuals who have over $100 million in wealth. Nobody is going to end up poor because of the “burden” of paying a reasonable tax. The second point is that short term investments are taxed as regular income. So the example isn’t great, anyway.

In spite of those caveats, it highlights the insignificance of the additional tax burden for capitalist speculators in volatile markets. Such a tax structure discourages hoarding and market manipulation while removing the loophole that the wealthiest individuals use to avoid most taxes altogether.