https://mas.to/@MikeBeas/113666556469008087

EDIT: I think you should get the service you pay for, just so that’s clear.

To make it easier to understand for our short term minds, let’s sketch a different scenario.

You hire a bodyguard. They’re a 7"2 giant bodybuilder with armor. Then someone walks towards you with a knife, raising it up and staring you in the eyes with a frantic expression.

Your giant bodyguard steps aside, and watches are you slowly get tortured to death. Little by little, while you scream for help. The bodyguard tells you Venezuelan blood torture is not covered.

I think someone might rightfully be upset with this bodyguard company. Perhaps as much as the health insurance company that forces people to go into a year long legal battle to get cancer treatment.

At least, that’s what I’ve been hearing about the healthcare system in the usa as of recent.

Any company that promises goods and/or services in exchange for money that takes your money in exchange said goods and/or services and then doesn’t deliver services or goods is a scam

I think that if money exchanges hands, it’s part of a deal that must be honored by the other party.

They’re getting very close to saying the quiet part aloud, and the quiet part is…

“Everyone except for the .0001% exists for the service of said .0001%, and the fact that you have any self-respect or value for your lives is a failing on your part peon!”

I would assume that I actually get a coffee when I go to Starbucks and pay for it.

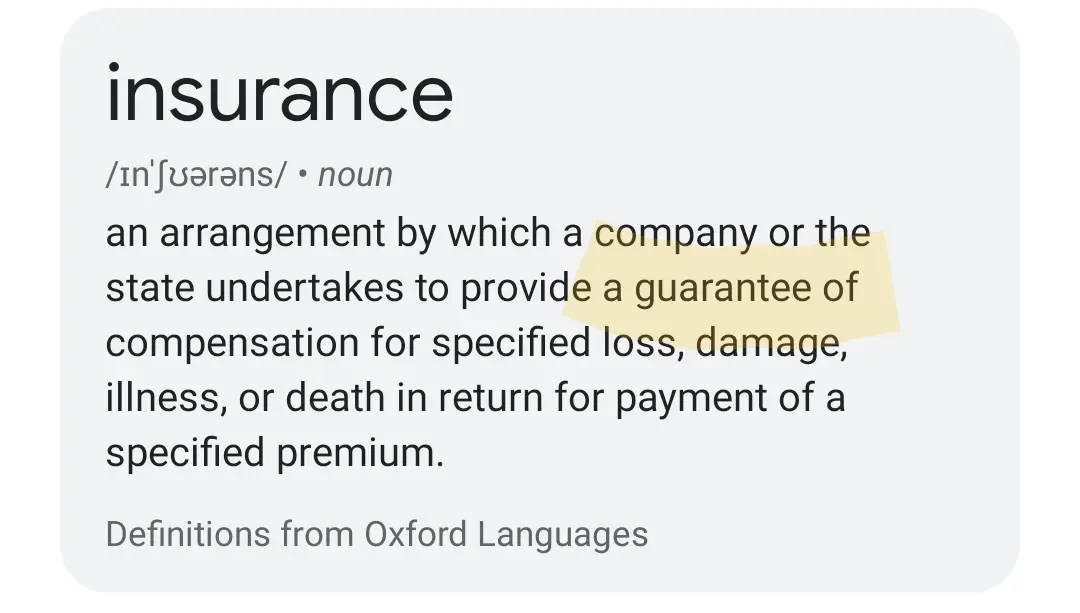

It doesn’t have to be a solemn vow. The definition of insurance is that it’s a guarantee. If it’s denying claims it’s technically not even providing insurance.

The customers of insurance companies are shareholders.

That’s not what a share holder is

You misunderstand. The service that insurance companies provide is one that is for shareholders. It’s a way of allocating and rationing medical care while also keeping business going.

Poor people don’t own hospitals. Poor people can’t develop medicines and medical equipment. Can’t train and hire doctors. That stuff is extremely expensive. The capital class owns that stuff, right?

They aren’t just going give it away are they? But they do need a labor force that, though desperate, isn’t too sickly that their labor can’t be exploited.

The service that health insurers provide to their actual customers, the capital class, is to reallocate the aforementioned expenses back onto workers by way of premiums and limiting care to the bare minimum.

This is why health insurance is tied to employment in America. You (most likely) didn’t hire your health insurer and negotiate your insurance contract, your employer did. It’s not for you, it’s for them, and really, for their owners, who extract the value of your healthy labor from your employer.

And this isn’t come an-cap or communist hot take, this is just the economics of how healthcare works in America. You’re getting the care, sure, and if you’re covered hopefully you’re in the road to recovery and won’t become insolvent due to medical debts, but this system is not for your benefit. It’s not out to save you money. You are at best an afterthought, a concept of a customer. More of a number.

The OOP described is, in different terms, as if health insurer was nothing more than a risk pool cooperative.

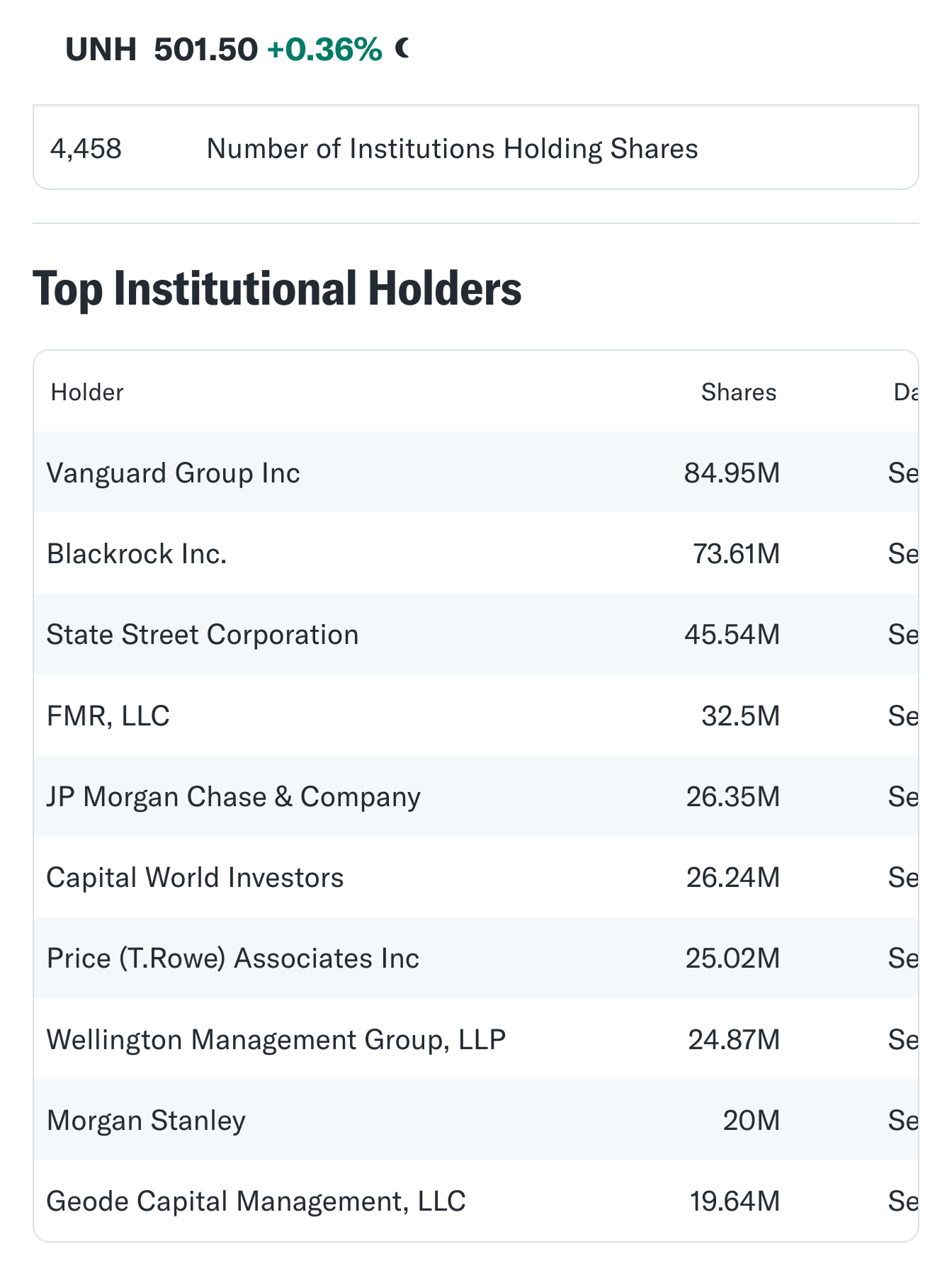

Here are the customers of UNH:

They also own the hospital groups, the device makers, and the pharmaceuticals.

If that’s the tack he wants to take with his argument, than in fact that opposite is true.

They’re a business. You provide them money and they provide a service. So in that respect, there should be no such thing as denial of service for ANYTHING because you’ve already paid for it.

What about the contract?

Well, what about the contract? Traditionally, contracts have three main elements: Offer, acceptance, and consideration. That is, one party offers something, the counter-party accepts the offer, and there’s an exchange of something of value between them. It ought to be obvious to even the most casual observer that there’s a lot to unpack about acceptance. Clearly, the party accepting the offer should understand the offer in order for the contract to be valid.

If I offer the neighborhood cats treats in exchange for not digging up my plants, and they accept, that doesn’t give me a cause of action to sue them (or their owners) for breach of contact when they still dig up my plants. A cat cannot lacks the understanding of the offer, and cannot accept, and therefore no contact exists.

Similarly, if a human lacks the mental capacity to understand an offer—say, a person deep in dementia agrees to a reverse mortgage without knowledge of their legal guardian—a court can rule that no contract existed, because the person did not understand the offer.

Health insurance contracts are anything but clear. In fact, the Byzantine details surpass the ability of most people to understand. (Part of my job in the past was getting paid to read and interpret health benefit statements for other people. Quick— what’s ERISA, and what are the legal implications of health insurance vs. health benefit plans?) Is it really a valid contract, if people can’t even begin to understand the offer?

One might say that people should get an attorney to look it over. Yeah, and then what? Counter-offer? We don’t have much leverage to do so, because the terms of all of the offers are bad, and opting out of health coverage entirely is not a good option. (Even the healthiest person could get hit by a car and be financially ruined for life.)

That’s the source of the anger. We can understand how insurance is supposed to work: Pay premiums to mitigate risk. Instead, these companies hide all manner of gotchas in contract terms we have no hope of understanding. Traditionally, that would not be a valid contract, but the legal system seems to exist to serve the powerful, so it enforces them anyway. (Even then, the insurance companies try to avoid fulfilling what seem like their clear obligations because sick people lack the wherewithal to fight them.)

Not giving you the coverage you pay for is theft. When are we going to normalize that and start putting CEOs in jail?

Only after revolution, share holders run the country, they wont allow us to cut into their grossly unnecessary wealth, they would rather we die.

Oblige them

Insurance is defined at its core as a transfer of risk. Its that simple. If insurance denies everything I send their way while I am paying them, its no longer a transfer of risk, I am simply paying someone to tell me ‘no’.

That out of the way, the whole health insurance industry does not follow the concept of transfer of risk. The insurance companies rather follow the concept of transfer of action. Basically I am not going to spend all day negotiating with a hospital. That said, them denying is because they do not want to do the work still, so in other words, I am still paying someone to tell me ‘no’.

In both concepts, the insurance companies are not doing what they ascribed to. Along with the laws that congress stripped away affordable care to its basics that we all are required to have it - read an extra tax but to corporations who give kick backs to their congressional lackeys - and the fact that insurance companies basically are price fixing all the rates and such, it becomes a lose (you)/lose (you)/lose (hospitals)/only ones who win are the companies.

Late stage capitalism hard at work.

I don’t care what that guy thinks.

Mike is not wrong. In fact, he’s very clearly laying out why insurance companies should not exist.

I’m not sure that was the argument he was trying to make though.

Do you guys think politicians have a duty to adhere to their campaign promises? They’re not under oath. They have no responsibility to improve anyone’s life. They’re a business to win votes to alter policy in their favour.

he’s very clearly laying out why insurance companies should not exist.

He’s laying the case for why insurance must either operate as a public loss-leader or a privatized scam. But I don’t think he really understands the bottom layer of the argument.

All I’m seeing is “Insurance is business. Business need to make money. Therefore denying claims is good aktuly.” There’s no “ah ha” bit at the end where he recognizes their predatory nature.

UnitedHealth Group is so vertically integrated that, in fact they do own doctors, hospitals and pharmacies under the Optum brand. So yes, they do have a duty to take care of people even if they act like they don’t.

This gaslighting won’t work anymore

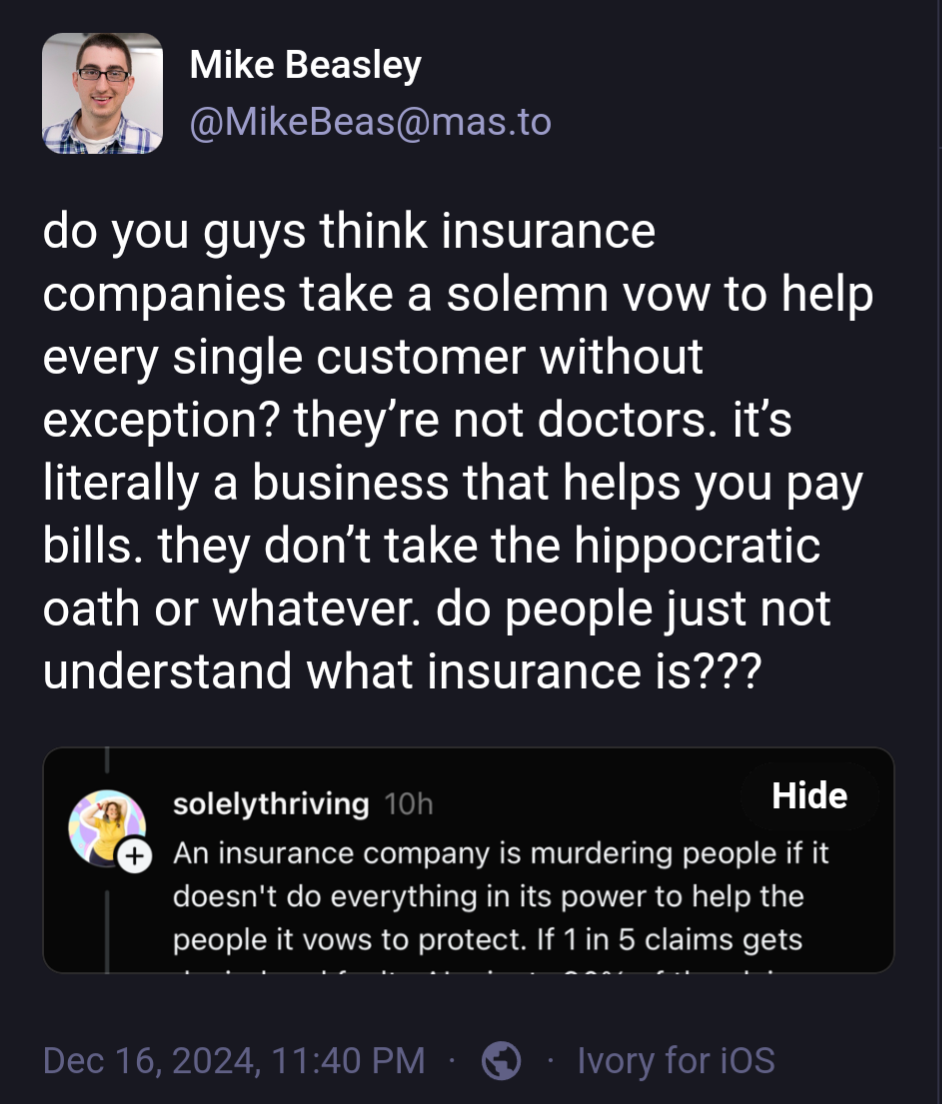

Insurance is a racket. Is that what Lil Mikey is saying?

it’s a business that helps you pay your bills

Quite the opposite, it’s a business that makes your bills expensive.

{kind=link}